Healthcare Reform Solves Nothing... It's The Debt, Stupid!

Zero Hedge - Sunday May 7, 2017

by Tyler Durden

Authored by Lance Roberts via RealInvestmentAdvice.com,

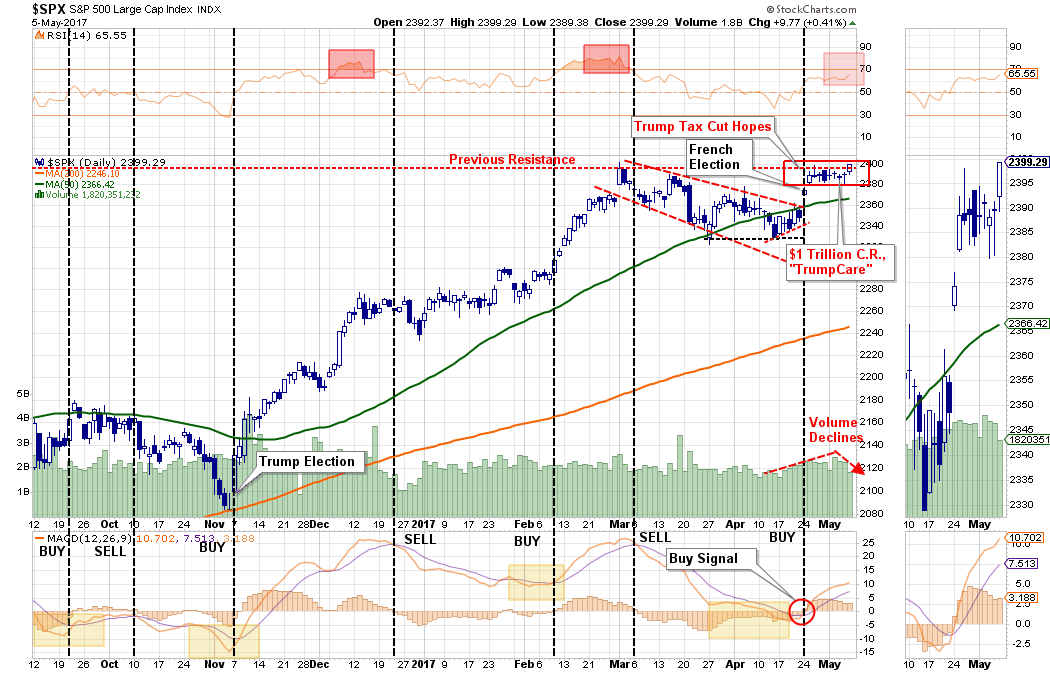

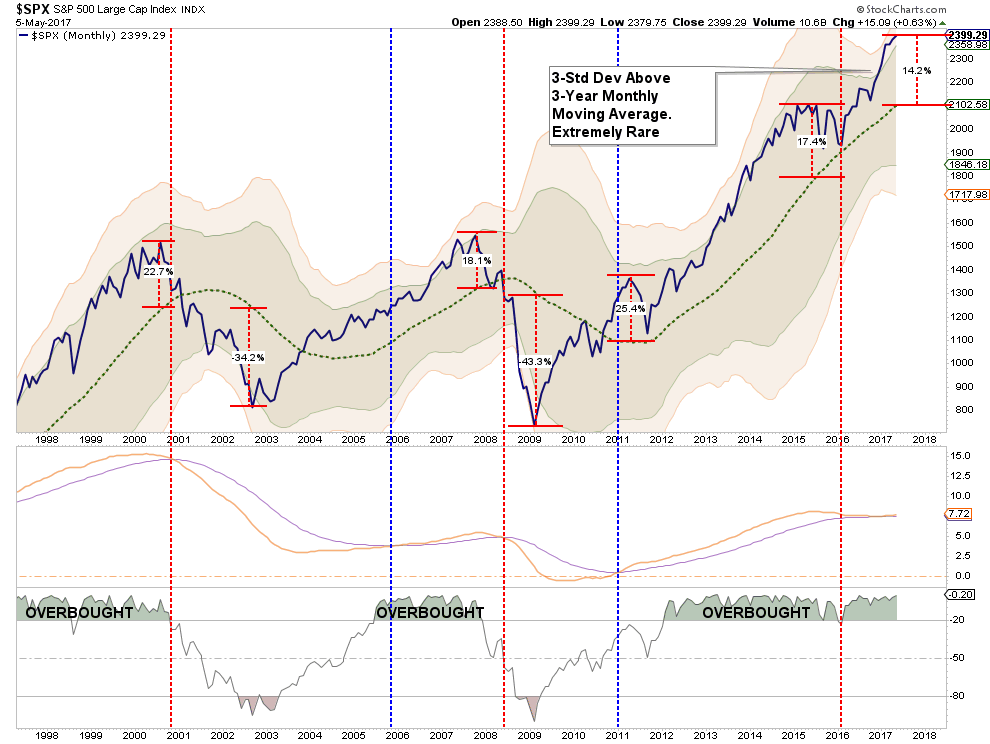

Over the last few weeks, I have been discussing the ongoing consolidation process for the S&P 500 from the March highs. (For a review read: “Oversold Bounce Or Return Of The Bull,” and “Return Of The Bull…For Now.”) As the expected rally in stocks, and reversal in bonds, took shape as the S&P 500 was finally able to ratchet a record close at 2399.29. (Read: 10/2016 – “2400 Or Bust”)

“With the market on a short-term ‘buy signal,’ deference should be given to the probability of a further market advance heading into May. With earnings season in full swing, there is a very likely probability that stocks can sustain their bullish bias for now.”

The market did do exactly that this past week, and while hitting a new high, as noted above, it was a “weak” breakout as volume contracted. My friend Dana Lyons made an interesting observation this past week:

You will notice that while such events did NOT rule out “new highs” first,such periods often preceded either mild or intermediate-term corrections.

Furthermore, despite the record close on Friday, it did little to change the intermediate term backdrop of the markets. The “warning signal” I discussed three weeks ago, still remains which is currently keeping a lid on stock prices for now. More importantly, we remain very close to triggering the secondary “sell signal,” also from an extremely high level, which would also raise caution levels higher, cut such has not happened…yet.

Importantly, both signals are improving over the last week, and, as I wrote last week:

“If the markets can continue to rally next week, and push to new highs, then both of those signals will reverse. The problem is the reversal from high levels historically has only been short-lived before a more significant decline took place as shown in the chart below.”

While much of the price action on Friday was due to continued “dovish Fed-speak” from a raft of speakers on Friday, it was also the high expectation of a successful French election this coming weekend. At current levels, the potential “reward” from an upward move next week is far outweighed by the downside risk.

Therefore, a “reactionary” approach to portfolio management is a better choice in the current environment. In other words, let the market determine our next course of action rather than trying to “guess” at what may happen. Throughout history, investors have rarely “guessed” well.

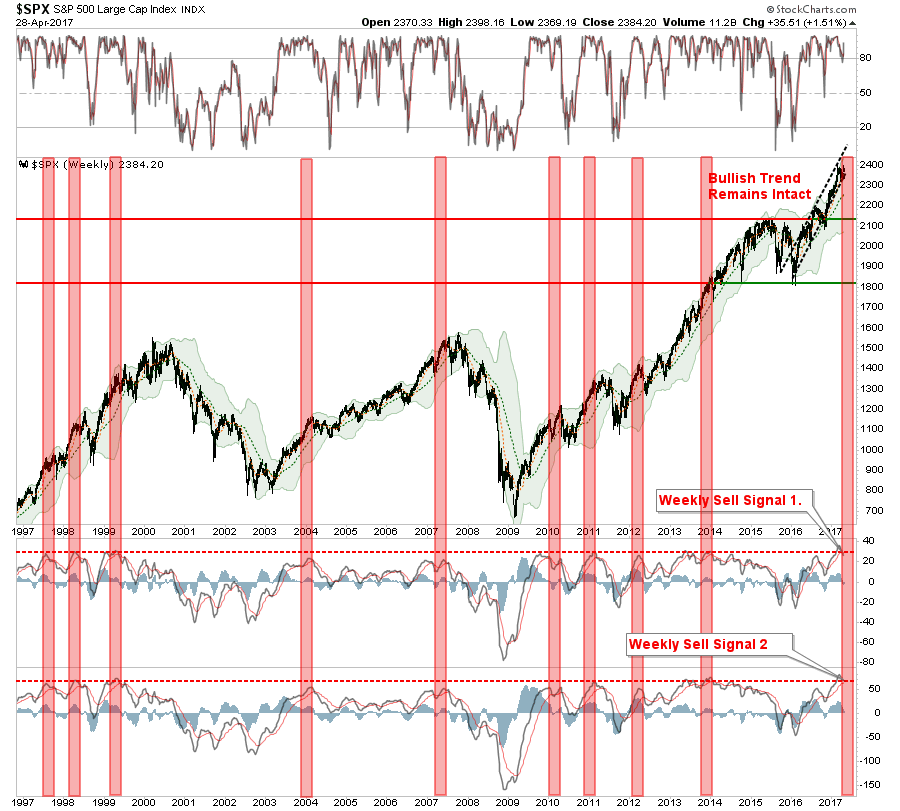

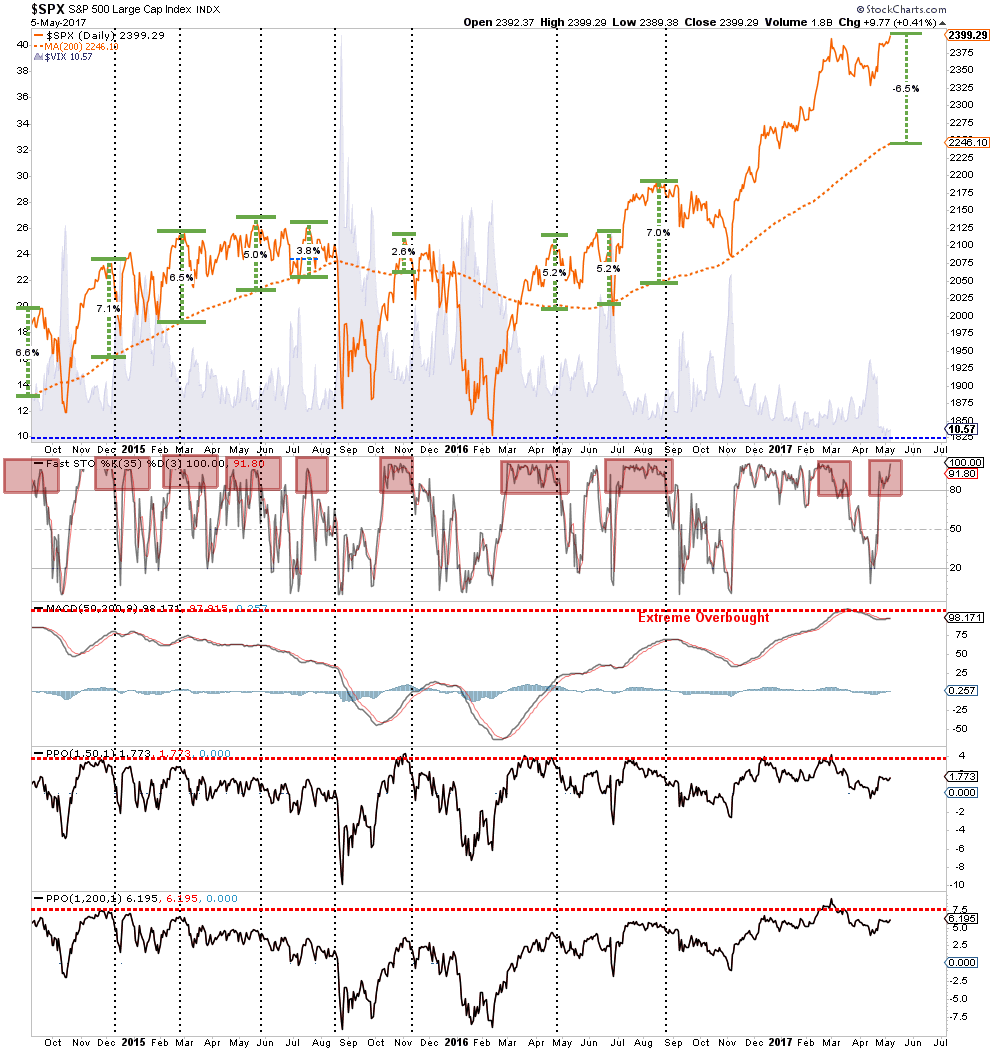

Despite the push higher this past week, it should be noted that since the beginning of March internal measures have remained weak. With the markets very extended above their 200-dma, a correction is likely over the next month or so. This is particularly the case as volatility has dropped to its lowest levels in recent history.

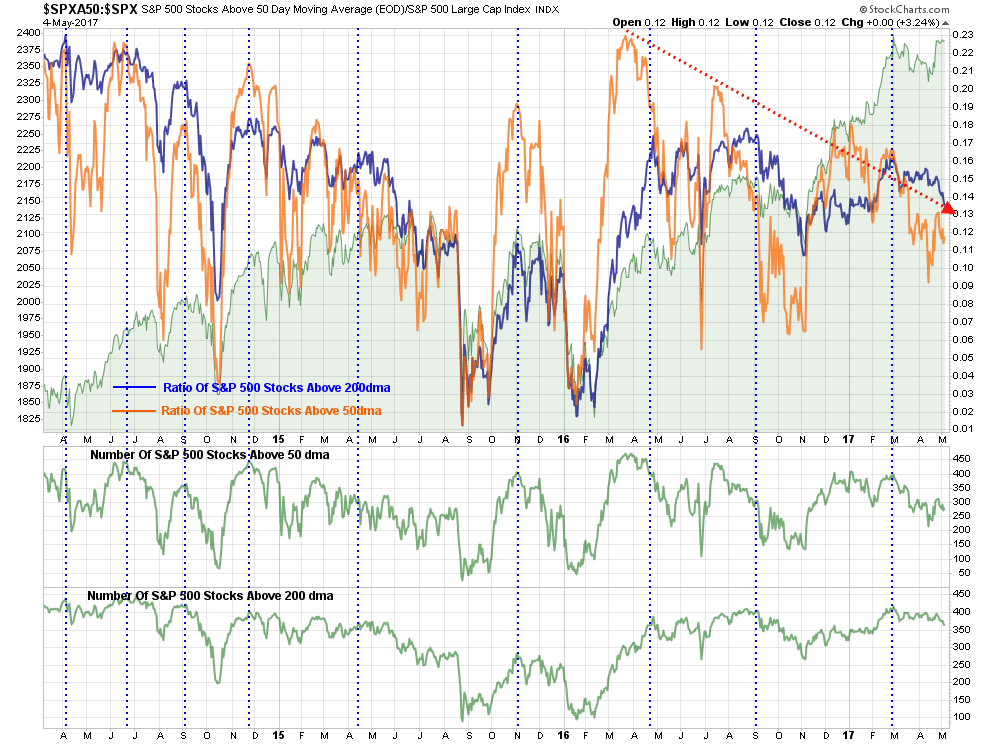

Furthermore, both the ratio and number of stocks above their respective 50 and 200 day moving averages has also remained weak.

Lastly, the market remains very 3-standard deviations above its 3-year moving average. While the long-term signal currently remains on a “buy,” it will not require much weakness sometime this summer to trigger a long-term “sell.”

For now, the market remains in a bullish trend which keeps portfolios allocated on the long-side. Outside of small tweaks and close monitoring, nothing has occurred, yet, which would warrant more drastic movements within the allocation model. However, we have reached a point in the market cycle where the “risk” of remaining heavily invested in the market far outweighs the potential “reward.”

As has been the case over the last couple of weeks, caution, nothing more, is advised for now.

AHCA Solves Little

First, everyone just calm the **** down.

The passage of the American Health Care Act by Congress this past week does nothing immediately. Nobody is going to die. No one will lose access to health care. The world will not end.

All that happens now is the bill moves to the Senate where it will likely be dead on arrival. Given the bill only passed by 4-votes in the House, there is a much narrower spread of leadership in the Senate. The bill will likely get tied up in debates, and even it does somehow miraculously get passed out of the Senate, whatever changes are made will likely lead to a loss when it returns back to Congress for a final vote.

Then we will get to restart this whole process over again.

This also means that tax reform, repatriation, and infrastructure spending are likely much further down the road than currently estimated.

One thing, however, is for certain – Obama no longer owns “the failed healthcare plan.”

It now squarely rests on the shoulders of President Trump and the Republican party. Since the current construction will increase healthcare costs and government debt, the opposite of why Trump was elected, it will likely cost Republicans control of House and Senate in the next election.

The ACHA, or now known as “Trump Care,” is roughly 90% ObamaCare with the taxes stripped out of it. Here are the details as provided by Goldman Sachs on Friday:

COVERAGE

- It would allow young adults to stay on their parents’ health plan until age 26.

- The bill would let states opt out of Obamacare’s mandate that insurers charge the same rates on sick and healthy people.

- It would also allow states to opt out of Obamacare’s requirement that insurers cover 10 essential health benefits, such as maternity care and prescription drug costs.

- The measure would provide states with $100 billion, largely to fund high-risk pools to provide insurance to the sickest patients.

- The bill also would provide $8 billion over five years to help those with pre-existing conditions pay for insurance.

- It would let insurers mark-up premiums by 30 percent for those who have a lapse in insurance coverage of about two months or more.

- The ability to charge older Americans up to five times more than young people. Under Obamacare, they could only charge up to three times more.

TAX

- The bill would end in 2018 Obamacare’s income-based tax credits that help low-income people buy insurance.

- These would be replaced with age-based tax credits ranging from $2,000 to $4,000 per yearthat would be capped at upper-income levels.

- The Republican bill would abolish most Obamacare taxes,including on medical devices, health insurance premiums, indoor tanning salons, prescription medications and high-cost employer-provided insurance known as “Cadillac” plans.

- Those taxes paid for Obamacare. Republicans have not said how they would pay for the parts of the law they want to keep.

- The bill would also repeal the Obamacare financial penalty for the 2016 tax year for not purchasing insurance, as well as a surtax on investment income earned by upper-income Americans.

- It would repeal the mandate that larger employers must offer insurance to their employees.

MEDICAID

- The bill would allow the Medicaid expansion to continue until Jan. 1, 2020. After that date, expansion would end and Medicaid funding would be capped on a per-person basis.

- State Medicaid plans would no longer have to cover some Obamacare-mandated essential health benefits, fulfilling a Republican promise to return more control to the states

The ramifications for the economy are not good. For investors it likely means a much longer wait for tax reform and the expected boost to corporate profitability. Per Goldman:

“In our view, House passage of the AHCA is likely to further delay the consideration of tax reform. House passage arguably reduces doubts that Republicans can assemble a working majority for controversial legislation in the House, which suggests that complex tax legislation might be achievable as well. However, since the House cannot act on tax reform using the ‘reconciliation’ process until the Senate has passed (or decides not to pass) its own health legislation, tax legislation looks unlikely to emerge until September in our view. Given the time it will likely take to reach an agreement on tax legislation, this suggests that enactment of tax legislation is unlikely until Q1 2018. While our base case is still that legislation is more likely than not to pass in 2018, further delays could push consideration of tax legislation too close to the upcoming midterm election, reducing the likelihood that tax legislation is enacted in the next two years.”

For investors, it is a case of “Waiting On Godot.” The only question is just how long will they wait.

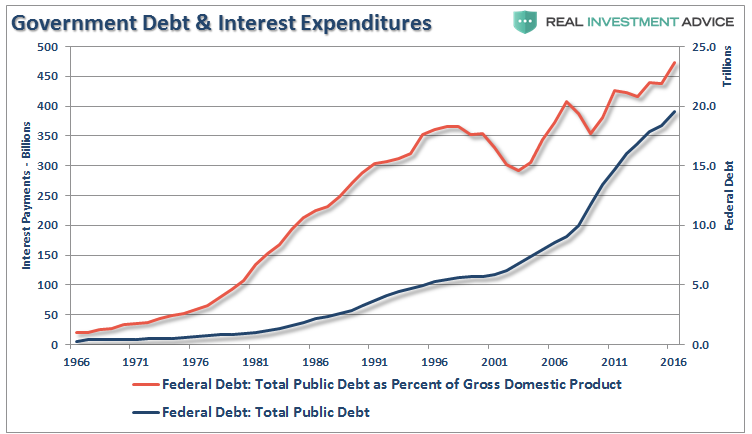

Debt Is The Problem

But of course, here is the bigger point.

The chart below is the current amount of debt (not including the $1.1 Trillion continuing resolution last week) and the amount of interest currently being paid on that debt.

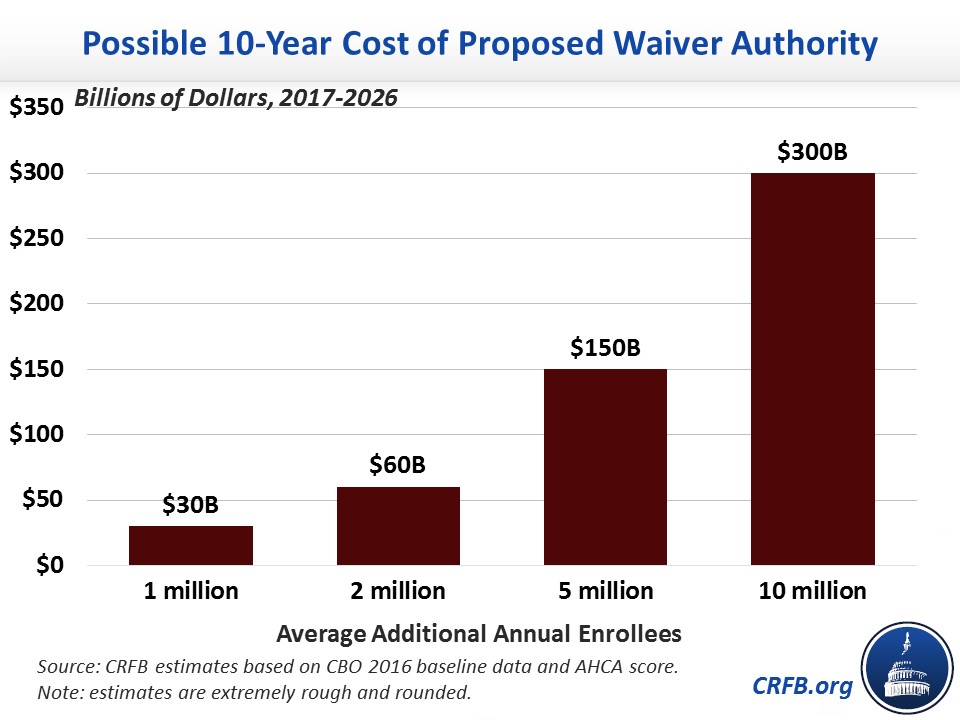

As the Committee For A Responsible Budget penned on Friday:

“Setting aside the health policy implications of these changes,the fiscal implications could be significant. If more people purchase health insurance, more will be eligible for the AHCA’s tax credits. Assuming no change in employer coverage, we estimate an increase of one million enrollees would cost about $30 billion over a decade, two million would cost $60 billion, five million would cost $150 billion, and ten million would cost $300 billion.”

“Taken together, that means the amendments would save an additional $5 billion if one million more people enrolled in insurance each year than CBO’s prior projection. But it would cost $25 billion if two million more people enrolled, $115 billion if five million more enrolled, and $265 billion if ten million did.With 6.5 million or more additional enrollees, the entire legislation would likely increase rather than reduce deficits.”

The significant importance of this was pointed out just recently in “Tax Cuts The Economic Growth Cure-All?”

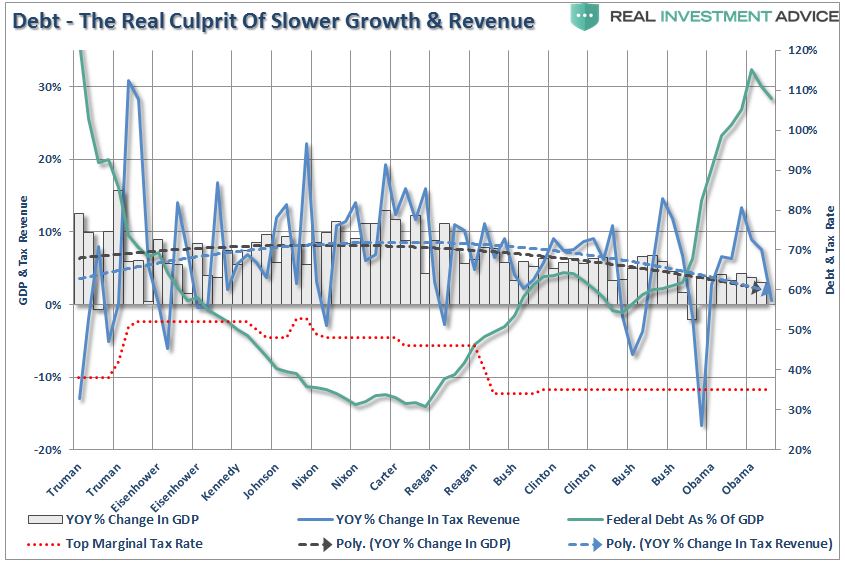

“Of course, as noted, rising debt levels is the real impediment to longer-term increases in economic growth. When 75% of your current Federal Budget goes to entitlements and debt service, there is little left over for the expansion of the economic growth.”

“The tailwinds enjoyed by Reagan are now headwinds for Trump.”

The true burden on taxpayers is government spending, because the debt requires future interest payments out of future taxes. As debt levels, and subsequently deficits, increase, economic growth is burdened by the diversion of revenue from productive investments into debt service.

This is the same problem that many households in America face today. Many families are struggling to meet the service requirements of the debt they have accumulated over the last couple of decades with the income that is available to them. They can only increase that income marginally by taking on second jobs. However, the biggest ability to service the debt at home is to reduce spending in other areas.

While lowering corporate tax rates will certainly help businesses potentially increase their bottom line earnings, there is a high probability that it will not “trickle down” to middle-class America.

While I am certainly hopeful for meaningful changes in tax reform, deregulation and a move back towards a middle-right political agenda, from an investment standpoint there are many economic challenges that are not policy driven.

- Demographics

- Structural employment shifts

- Technological innovations

- Globalization

- Financialization

- Global debt

These challenges will continue to weigh on economic growth, wages and standards of living into the foreseeable future. As a result, incremental tax and policy changes will have a more muted effect on the economy as well.

Read More Here

No comments:

Post a Comment